While it depends a little on which residency or citizenship by investment scheme you apply to, most programmes offer whole family eligibility, with each individual granted a second passport or residency status. The age of the dependents varies from program to program – please check this with one of our consultants. That includes options to add a spouse or civil partner, dependent children, parents, sometimes siblings and grandparents to your application.

Astons has years of expertise expediting immigration by investment applications, with some of the opportunities allowing you to acquire a second passport in as little as 30 days! Other programmes require around three to four months. Some have phased citizenship with an initial residency period – although several investment schemes have the option of securing fast track processing for a nominal charge if you would like to relocate or secure a second passport faster.

Citizenship by investment offers an exceptional way to invest in emerging economies, sought-after property markets and businesses. Most second passport schemes require you to retain your investment for a minimum period, usually up to five years. However, when that period has passed, you can sell your investment to recoup the capital, often making a sizable profit in addition to returns earned in the meantime. If you opt for a non-refundable government donation route, then the value is not recoverable.

Once you have a second passport, you don’t need to do anything further to retain your citizenship other than comply with any requirements to maintain your investment for a certain number of years. When your passport falls due for renewal, you can request a replacement through the regular passport processing system in that country. Alternatively, please contact Astons if you need any assistance finding the quickest way to renew a second passport when the original expiry date is approaching.

A second passport is valid for life – you remain a citizen of that country indefinitely, with most citizenships passing down to your descendants. The only reason a passport might be revoked is if you breached a fundamental term of citizenship or residency program (such as selling your investments earlier than required by the program) or committed a serious offence in the country that issued the document.

Every country with a residency by investment or second citizenship scheme has benefits and incentives on offer. The differences include:

• Types of investment – ranging from property purchases to charitable donations.

• Invest thresholds – starting at $100,000 for Caribbean second passport schemes.

• Terms – you might not need to retain an investment or may need to keep a real estate acquisition for between three and five years.

• Travel rights – our supported programmes offer generous visa-free travel, including to prestigious destinations throughout Asia, Europe and the United States.

The Astons website includes detailed information for you to compare different immigration programmes, or our friendly team is always available to offer advice.

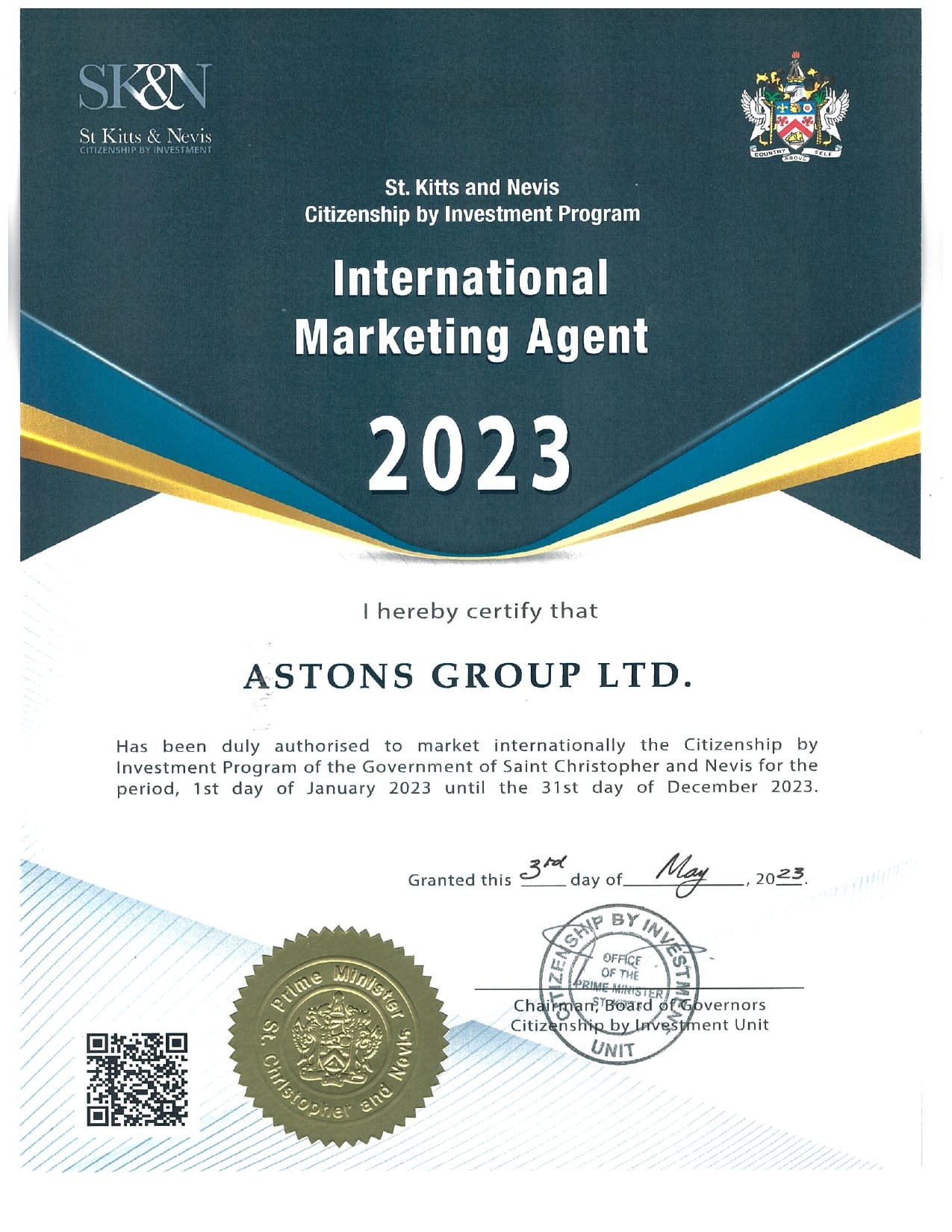

Astons is an officially recognized marketing agent of the Citizenship by Investment program of Saint Kitts and Nevis. The Government of this Caribbean country trusts us to process the documents of future citizens of Saint Kitts and Nevis and transfer their applications for a passport.

We are permitted to promote, market, and assist our clients in obtaining Grenada citizenship. We are licensed to submit applications to the government under the program.

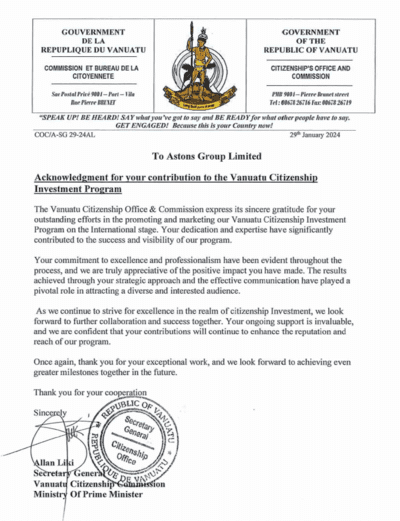

Astons is a trusted authorised Vanuatu Citizenship Agent, we deal directly with official representatives. Our expertise means that we can act as one of the few authorised agents able to apply for citizenship on your behalf.

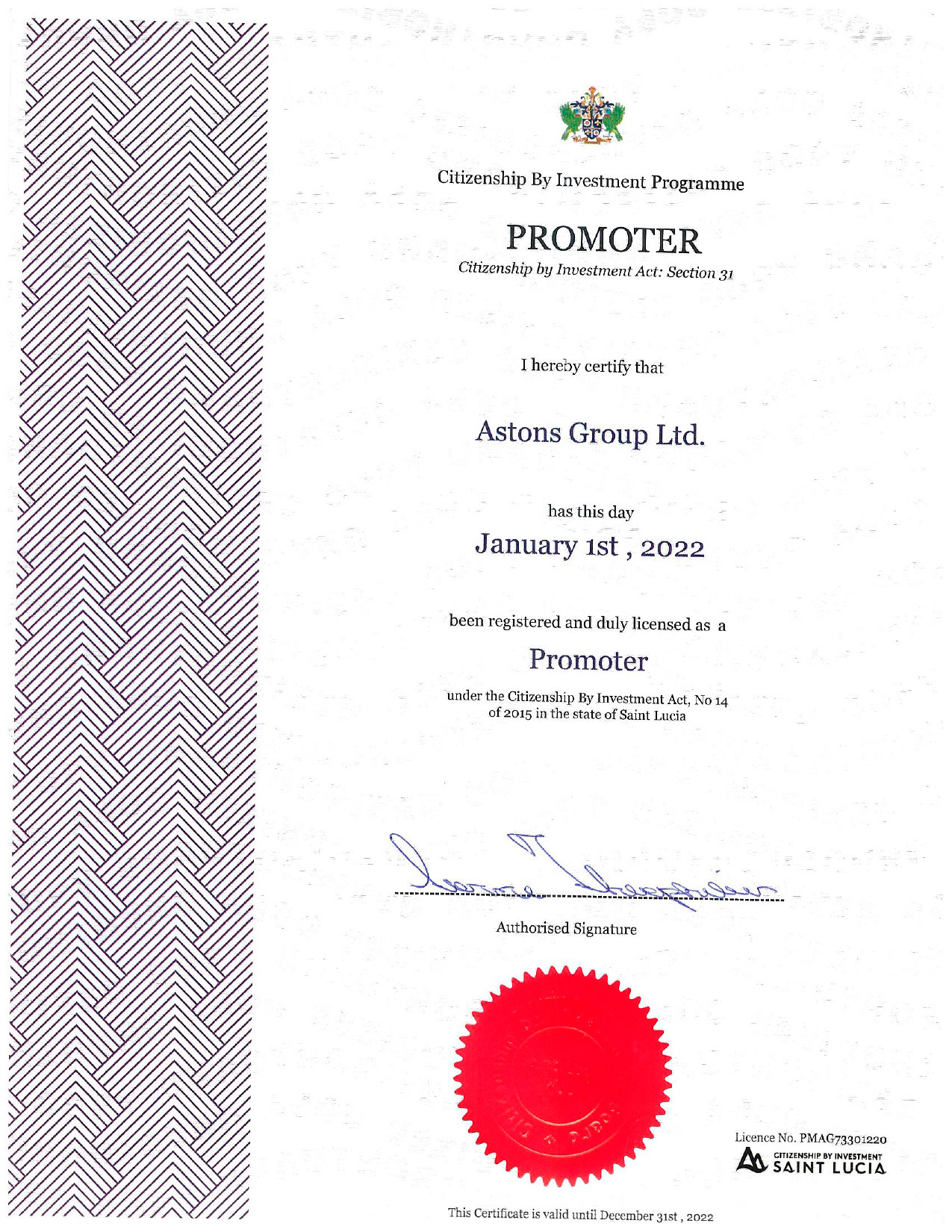

Saint Lucia Citizenship by Investment – the most affordable citizenship program from $100,000.

USA

UK

UAE

Turkey

Cyprus

Greece

Portugal

Malta

- USA

- UK

- UAE

- Turkey

- Cyprus

- Greece

- Portugal

- Malta

Contacts

Show on map

Alena Lesina

Citizenship, residence permit and real estate investment expert in USA

Contacts

Show on map

Yulia Zabyshnaya

Citizenship, residence permit and real estate Senior Advisor

Contacts

Show on map

Igor Nemtsov

Citizenship, residence permit and real estate investment expert

Contacts

Show on map

Contacts

Show on map

Denis Kravchenko

Astons Business Development Director and Head of Astons Cyprus Office

Contacts

Show on map

Contacts

Show on map

Susanna Uzakova

Citizenship, residence permit and real estate investment expert